Decoding private capital’s BPA play

Public markets have been mispricing UK life insurers, and private capital has spotted the arbitrage. Full slides and transcript from my talk at the Westminster and City conference, 28 April 2026.

Note: These are my personal views only and do not constitute investment advice. See full disclaimer below.

Audio embedded below.

On 28 April I spoke at the Westminster and City conference in London, the largest bulk annuity gathering of the year. Around 420 people filled the room this year, drawn from across the world: the big consultants and actuaries, the listed insurers and BPA specialists, the global asset managers, the magic-circle law firms, and a heavy contingent of Bermuda reinsurers and North American life groups. The Bermuda Monetary Authority was there, alongside the PRA and the Pensions Regulator.

This was my third time speaking here, and the audience has grown each time, so they keep having to find a bigger room. The brief was simple. Other speakers would explain what the private capital players are doing. My job was to explain why.

When I was at RBC Capital Markets, I started a bulk annuity conference of my own, back in 2013, and used to chair it. This time the roles were reversed: I was in the speaker's chair, and the chair of this year's conference was one of the speakers I used to book at mine all those years ago. Ever since that first conference in 2013 I have argued that the UK bulk annuity market is the best structural growth opportunity in European insurance, and that investors have consistently mispriced it. The view I took to the room this time is the same one I have been writing on Substack for months: public markets have been pricing these businesses wrong, and private capital has spotted the arbitrage.

What follows is the full set of 16 slides, with my speaking notes underneath each one. The slides do real work in this talk. They carry the data on the deals, the rally, the dividend yields, the spread arithmetic. The transcript has been lightly edited to read smoothly on the page; the argument is exactly what the W&C audience heard.

Thank you, and good morning. The view I am going to give you is from the listed equity market, the market that private capital has just exposed. Other speakers will tell you what the private capital players are doing. I am going to tell you why. The short answer, which I will spend the next 20 minutes proving, is that public markets have been pricing these businesses wrong, and private capital has spotted the arbitrage.

Foreign capital is reaching into UK life insurance. US and Canadian hands into the UK life cash pile. That is the whole story in one picture.

You know the deals already. Athora and PIC, £5.7bn, completed end of March. Brookfield and Just, £2.4bn, completed beginning of April. These are not toe-in-the-water deals.

Look at who is on the pitch. Apollo, Brookfield, Blackstone, GIC. The heaviest pools of capital on the planet have decided UK life insurance is mispriced.

This is not new globally. The US saw the same pattern a decade ago. The UK has reached the same tipping point.

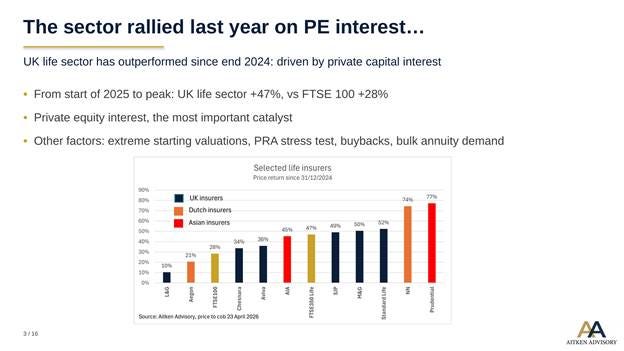

The market certainly noticed. The chart shows share price performance since the start of 2025. The UK life names are in dark blue. The FTSE 350 Life sector is at +47%; the FTSE 100 is at +28%. That is 19 percentage points of outperformance.

A lot of the re-rating came ahead of the deal announcements. The narrative that private capital was interested built quickly, and share prices moved on the narrative as much as on the news. In my view, PE interest was the single most important catalyst. Other factors that helped were the extreme starting valuations, the PRA stress test landing better than expected and continued BPA demand.

I remember the first time I spoke at this conference, seven or eight years ago. Chatting to people in the coffee break before my talk, I got the sense everyone was so positive about the sector. So I opened my talk with the point that if I dropped down from the moon and listened to the room, I would think these stocks were on 30 times earnings. They are not, and never have been.

Even after last year’s lift in share prices, the sector is still cheap. I have spent my career being told by institutional investors why, and that is what the next 10 minutes are about.

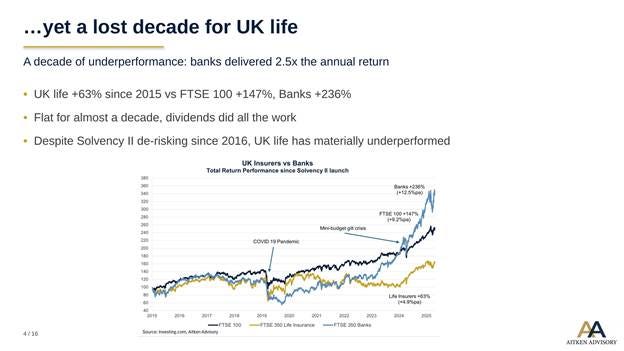

Zoom out from the 2025 rally and take it back to the end of 2015, when Solvency II was about to come in. Since then, banks have more than tripled, the FTSE has more than doubled, and the life insurers are up just 63%. Banks have delivered roughly two and a half times the return of UK life.

Strip out the dividends and the life sector is flat in price terms. Solvency II came in at the start of 2016, and the sector de-risked materially on the back of it. Balance sheets became much safer; equity markets did not reward that at all, in fact quite the opposite.

The 2025 share price lift sounds dramatic. Set against a decade of no progress, it is merely a catch-up. The valuation gap is still wide, which is why the private capital interest has not stopped.

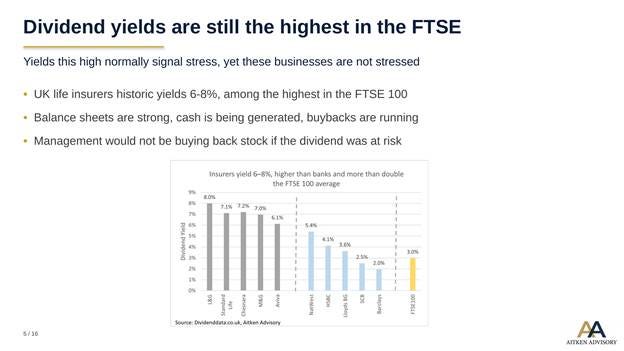

Look at where this has left us. Historic dividend yields of 6 to 8% across the UK life sector, among the highest in the FTSE 100. L&G’s historic yield is 8% and is one of the very highest yielders in the index. The FTSE 100 average is 3%.

Every single UK life insurer has a higher dividend yield than every single UK bank.

Yields that high normally mean one of two things: the dividend is about to get cut, or it will not grow. Solvency ratios are at record levels, so this is clearly not distress. Balance sheets are strong, cash is being generated, buyback programmes are running. Management teams would not be buying back stock at these levels if they thought the dividend was at risk.

Brookfield came to the same conclusion when they paid a premium for Just.

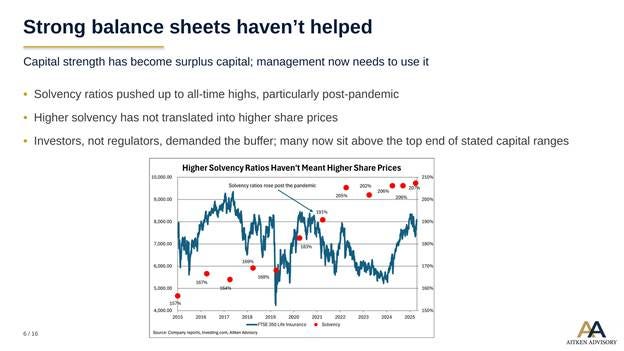

Solvency ratios have been pushed up to all-time highs, particularly post-pandemic. You can see that from this chart. I’ve plotted the price return for the sector. The red dots are the average solvency ratio. The average at end 2025 was 207%.

The insurers mostly all sit comfortably above their stated capital ranges. It may surprise you that the regulator is not asking for more; in my experience investors asked for it, and the companies have responded. When I ask insurers why 180% is the right number for the top of their range, they almost never tell me it is to guard against a 1-in-X event. They say there is an element where ‘we have looked at peers, and that is where everyone is sitting’. The ranges are peer-driven, not loss-driven.

The problem is that the Solvency II internal models are stochastic and so complex that investors cannot really have a sense of what the right number is. It is just a number to them, so they push for forever higher. The result is that balance sheets, in my view, are now too strong; with too much capital, the return on capital is lower.

Private capital’s read is simple: if public markets will not reward the balance sheet, we will buy the balance sheet.

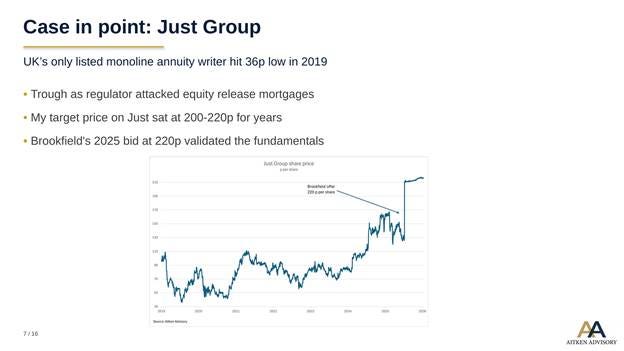

Just Group is the best example of how public market investors view the bulk annuity market: the only listed pure-play, monoline BPA writer. As an equity research analyst, I liked the bulk annuity market, liked the stock, and thought management would execute. The shares were so low for so long it was so tough to push as a Buy. A big factor was the regulator turning on equity release mortgages in 2018, and Just was the most exposed. The market decided the franchise was broken. In my view, it was not broken at all.

The shares fell to 36p in 2019, and I had a target price of 200 to 220p the whole way through. When you start at an investment bank, you get told not to go too extreme on price targets, because investors will disregard your view as coming from an idiot. I broke that rule on Just.

With the shares below £1 and my target above £2, a very senior analyst, a competitor, cornered me in a lift and told me I was risking my career and reputation. I stuck by it.

Brookfield then came in at 220p in 2025. A private capital buyer had concluded the listed price was wrong. Unfortunately I had left the sell-side by then, so I did not get the credit! The valuation gap is not just theory; a very large professional investor has just written a very big cheque to prove it.

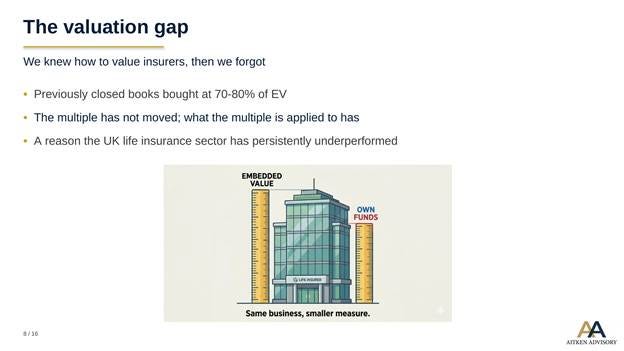

Why has the gap opened in the first place? Part of the answer, I think, is that we lost something when we dropped embedded value, and I have been writing about this on Substack recently.

Over the years, the deal or valuation multiple has not really moved; what the multiple is applied to has. Just over 20 years ago Clive Cowdery built Resolution buying closed books at 70 to 80% of embedded value. That was the template. When deals are priced now, they are quoted in multiples of unrestricted Tier 1 own funds. The multiples look very similar to the EV-era multiples, yet in almost every case, embedded value is a higher figure than own funds. Same multiple, but applied to a smaller number.

In practice investors probably do not really understand either metric, so they apply the old multiple and move on. The result is that insurance company valuations have quietly gone down.

The sector has a real problem with complexity, and it does not, as a rule, do a good job of explaining how it makes money. It is why I started my Substack newsletter Breaking Down the Insurance Black Box.

Unless you are at one of the very largest fund managers, you tend to have one person covering all of financials. Over my career the same thing has come up. They tell me, ‘I understand banks, I understand asset managers, I do not understand life insurance, so I will stay away.’

The sector has to do much more to simplify. Three accounting frameworks run in parallel: IFRS 17, Solvency II and EEV, each giving a different answer for the same year’s profit. Annual reports are full of jargon. Even this results season, every single life company that reported, without exception, was marked down a lot on the day. There are so many metrics in play that there is always one number the market can pick on.

Compare that to other sectors. I know a buy-side insurance analyst who also covers other sectors. He says that in a non-insurance sector you can have 10 analysts on a stock and they will universally say the results were good, or universally bad. In insurance you get five saying good and five saying bad on exactly the same results. Private capital buyers can understand the jargon, and that is the edge.

I have polled my clients about what they don’t like about the sector. They come up with a long list of worries, but number one is always asset risk, which is credit risk. They worry that insurers are in risky assets which will default.

Then come the operational worries: regulatory risk, by which I mean the PRA’s perceived appetite for tightening, and new business strain. Bulks are capital intensive up front, which the market reads as a cash drag.

Then come the tail risks: run-on as an alternative to buyout, superfunds, and longevity improvements running ahead of reserve assumptions. Each is legitimate, yet none has materially impaired a UK life insurer balance sheet since 2003.

I always see the 2000-2003 bear equity market as the big life insurer crisis. Assets and liabilities were not matched back then. Serious lessons were learnt, matching was introduced, and there have not been any major issues since.

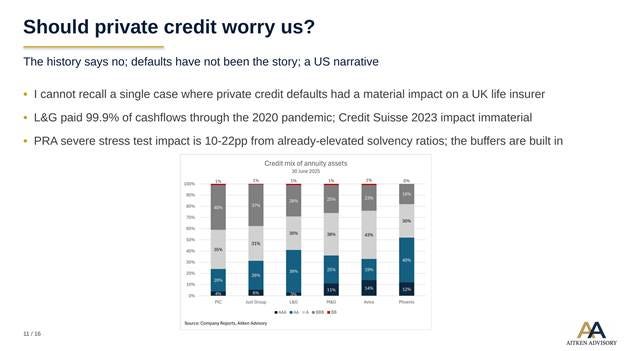

Private credit is the current asset-risk worry. When Jamie Dimon talks about cockroaches, the market gets spooked: when you see one cockroach, there are probably more. He was referring to private credit. UK life insurers do invest in private credit, so the worry is not invented. The danger is importing a US narrative that is, in fact, a very different story.

Three things separate UK BPA private credit from its US cousin: regulation, instruments and supervision.

The regulation argument starts with the matching adjustment. Solvency II in practice forces UK BPA portfolios to be cashflow-matched, investment grade and held to maturity; the US framework is state-by-state and far less prescriptive.

On instruments, UK BPA private credit is mostly infrastructure debt, social housing, secured property and equity release, all secured, long duration and investment grade. The US worry is middle-market leveraged loans, a fundamentally different risk.

Supervision is the third gap. The PRA does not request cooperation; it establishes itself in your office until satisfied.

Over 20+ years in this sector, I cannot recall a credit default materially hitting a UK life insurer’s capital position; roughly 99% of annuity portfolio assets are investment grade. Credit Suisse in 2023, the biggest banking casualty of the decade, had next to no impact on UK life insurers, and the sector sailed through last year’s PRA stress tests.

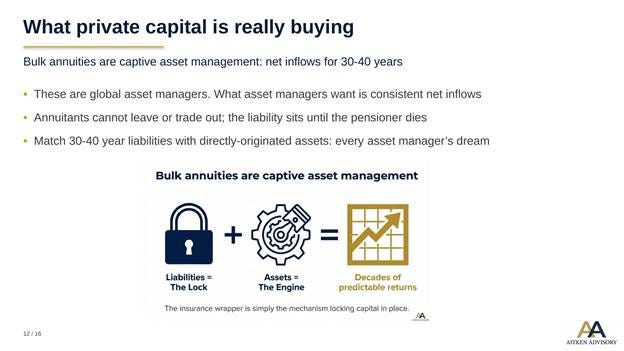

Step back, and what private capital really is, is global asset management. What every asset manager wants is consistent net inflows.

The structural problem with traditional asset management is that net inflows follow performance. When performance is strong the inflows turn up; but when performance turns south, the inflows go south too, and quickly.

Bulk annuities are fundamentally different. The market gives you positive net inflows for 30 to 40 years, with no outflows. If you are a pensioner in receipt of an annuity, you cannot move it, and you cannot cash it in. It sits with you until you die.

A buyout is a very big net inflow. Pension trustees hand over the assets, the insurer takes on the liabilities, and the money does not leave. You end up with a 30 to 40 year book of liabilities and a continuous stream of net inflows. That is the dream book for any asset manager, and it is what private capital is really buying.

The lazy narrative is that private capital takes more risk for more yield, and pensioners suffer. But the PRA will not allow that; the matching adjustment will not allow that. The BPA regime stops insurers reaching for risk to improve spread.

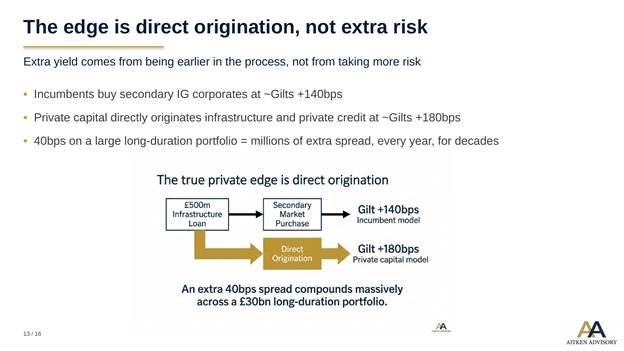

Extra yield comes from two places: more risk, or being earlier in the process. Private capital is doing the latter, not the former. The incumbent buys secondary-market corporates at, say, Gilts +140bps. Private capital directly originates infrastructure loans, private credit and structured real estate at the same investment grade rating, at Gilts +180bps. They are paid for the origination work the secondary market does not do. That 40bps is sourced, not borrowed: not leverage, not subordination, not a worse credit. It is the spread for structuring the loan.

40bps on a £30bn long-duration portfolio is £120m a year, every year, for decades.

Compounded over the life of the liabilities, that is billions. Listed UK life insurers cannot match this without owning the origination engines. The message is simple: they need to up their game.

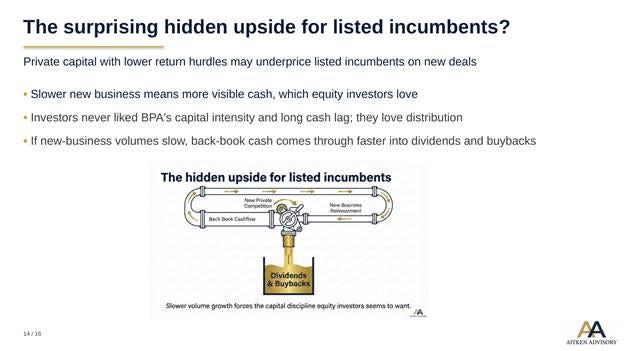

Let me close the circle. There might actually be hidden upside for the listed incumbents from all of this.

Going back to my client conversations, one thing investors have never liked about BPA is the lack of cashflow. The model for years has been that cash off the back book gets reinvested into writing new business, so BPA as a whole has not really seemed to generate cash for shareholders. Investors love dividends and buybacks, especially these days.

Here is the counter-intuitive bit. If new business volumes at the UK life names slow because private capital is taking share, then back-book cashflow comes through more visibly into dividends and buybacks, rather than being ploughed back into new-business strain. Slower growth, and faster distribution. That is probably good for listed share prices, even though it is the opposite of what you would expect.

Let me close with three points.

One, unsurprisingly, private capital has come into this market. Bulks are a great product: high growth, highly profitable. The push reflects a public-market pricing error, not a break in the insurance model.

Two, it sounds slightly crazy, yet private capital can take a longer-term view than the public markets. Public-market investors are pinned to three-year horizons, so private capital is the patient money here. I cannot promise a three-year re-rating, but over 10 to 20 years I expect the UK life names will do very well, because dividends keep coming and risks do not.

Three, on the history, dividends are covered, balance sheets are strong (maybe too strong), and through every crisis (2008-09, Brexit, the pandemic, the Middle East) the sector has been fine. This is fundamentally different from the banks. Life insurers do not need to sell assets in a crisis: the liabilities are illiquid, the annuitant cannot run.

Share prices get marked down, yet the businesses are absolutely fine.

More crises will come, the sector will be fine, and that should show up in share prices.

That is where I closed at the conference.

Since the talk

The month since I spoke has been a decent one for the sector. Over the past 30 days L&G is up around 6.5%, the clear outperformer on the bid speculation, with Chesnara up 4.4%, M&G up 3.5% and Standard Life up 1.8%. Aviva is down 2.2%, and the FTSE 100 itself is broadly flat.

29 April 2026: the PRA reprices funded reinsurance. The day after I spoke, the PRA spoke at the same conference and published consultation paper CP8/26, raising the capital held against the average funded reinsurance trade from 2-4% of liabilities to around 10%. This is good news for the listed sector, in my view. The regulator has removed the cheap-capital lever that drove the BPA price war, which should mean more pricing discipline and, over time, better margins on the business actually written. (See my piece: The regulator doesn’t do favours, this time it did)

Late April 2026: Standard Life is reported to be bringing in private capital. The FT reported on 22 April that a CVC and Prudential Financial consortium is frontrunner to put more than £1bn of equity into a new bulk annuity vehicle inside Standard Life, alongside its £2bn purchase of Aegon UK. If this deal happens I see it as likely good for the share price in the near term, but I do not think it is good for earnings over the long term: the listed shareholder ends up with a smaller slice of the better business, the 20%-plus IRR annuity book, and a larger slice of the worse one, the DC platform. I called it a quiet concession that the listed market is the wrong place to own UK BPA economics. (See my piece: Is Standard Life about to trade 20% IRRs for a re-rating?)

14 May 2026: L&G comes back into play. The FT asked whether L&G would be "the City's next domino to fall", reporting that several US private capital firms are drawing up bid plans, with one source saying people are now spending real money on it. The CEO said there were no discussions, and the shares rose 6.2% anyway. Compress L&G's 8.6% prospective dividend yield to the 5% Allianz trades on and the implied price is around 453p, a 71% premium. A full bid would reprice the whole listed sector overnight. (See my piece: 27 years on: is L&G back in play?)

26 May 2026: the pattern, over 30 years. I set this wave against my own career, from losing Resolution to a sharper-eyed buyer in 2007 to the PIC and Just takeovers this spring. Across five eras the same UK life books keep changing hands at a discount, and only the type of buyer changes; today it is the global asset managers. The public market has never quite believed what these businesses are worth, and being attractively priced is exactly what keeps putting them in play. (See my piece: I Lost Resolution in 2007. The Professional Buyer Keeps Winning)

Gordon Aitken runs Aitken Advisory, providing strategic advice on UK and European life insurers and pension funds. I work with investors, insurers and advisers on transactions, capital strategy and market positioning. As I did throughout my sell-side career, I meet fund managers and investors for one-to-one briefings on the sector. If you would like to arrange a briefing or discuss a potential engagement, click the button below to email me.

Want a deeper dive on UK life insurers, annuity balance sheets, and why markets often misprice them in stress? That is the core theme of my book, Breaking Down the Insurance Black Box.

Disclaimer

The content of this publication reflects my personal views only and is provided for information purposes. It does not constitute investment advice or investment research, and I am not acting in the capacity of an investment adviser. I own shares in some of the companies mentioned. Readers should carry out their own analysis or seek professional advice before making any financial decisions.